All Categories

Featured

However, these policies can be extra intricate compared to other kinds of life insurance policy, and they aren't always appropriate for every investor. Talking to a seasoned life insurance policy agent or broker can help you make a decision if indexed universal life insurance policy is a good fit for you. Investopedia does not supply tax obligation, financial investment, or monetary services and advice.

, adding an irreversible life plan to their investment portfolio may make feeling.

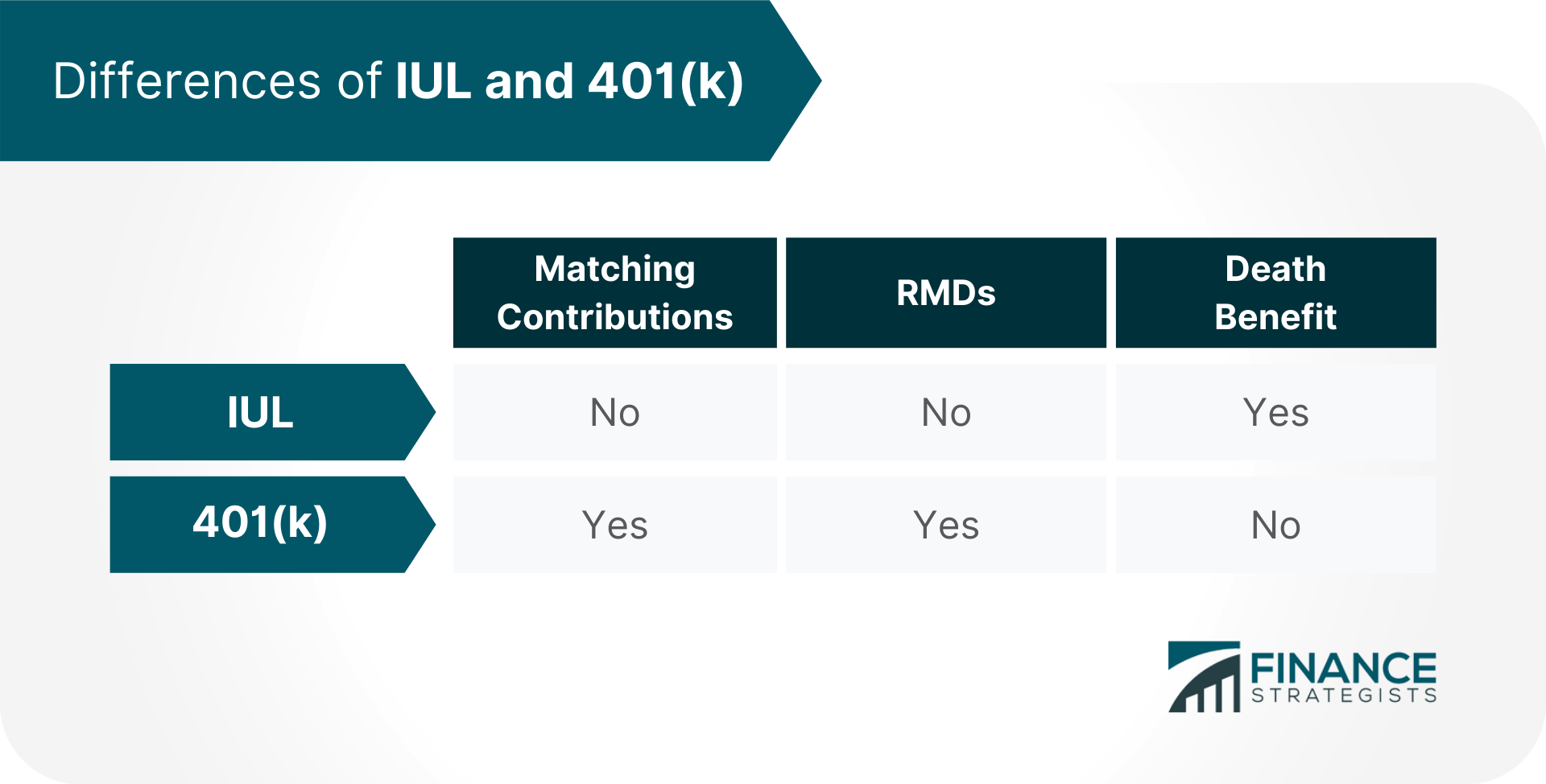

Reduced prices of return: Recent research study located that over a nine-year period, staff member 401(k)s expanded by approximately 15.6% each year. Contrast that to a set rate of interest of 2%-3% on an irreversible life plan. These distinctions accumulate in time. Applied to $50,000 in savings, the fees above would certainly equate to $285 per year in a 401(k) vs.

In the very same vein, you could see investment growth of $7,950 a year at 15.6% passion with a 401(k) contrasted to $1,500 per year at 3% rate of interest, and you 'd spend $855 even more on life insurance policy each month to have entire life coverage. For lots of people, getting permanent life insurance coverage as component of a retirement is not a good idea.

Iul Nationwide

Below are two typical kinds of irreversible life policies that can be made use of as an LIRP. Whole life insurance policy offers dealt with premiums and cash worth that grows at a set rate set by the insurance firm. Traditional investment accounts typically use higher returns and more adaptability than entire life insurance policy, but entire life can offer a fairly low-risk supplement to these retired life savings techniques, as long as you're certain you can afford the premiums for the life time of the plan or in this instance, up until retirement.

{kind=link}

Latest Posts

Infinite Banking Real Estate

Be Your Own Bank - Infinite Growth Plan

Life Insurance Banking